A stablecoin sitting in your wallet earning 0.1% a year feels like a waste, so the moment you see a platform offering 12%, 17%, or even higher on the same coin, it is tempting to move everything over immediately. The problem is that yield numbers on their own tell you almost nothing about whether your money is actually safe. Two platforms can both advertise "17% on USDC" and mean two completely different things, one backed by a regulated custodian with insurance and daily audits, the other running on thin reserves that could freeze withdrawals the moment redemptions spike. Knowing how to separate the two is the single most important skill for anyone parking stablecoins for yield.

Why the headline rate is the least useful number

Platforms know that a big percentage sells. So many of the highest rates you see advertised are promotional tiers, not the base rate you will actually earn long term. A platform might offer 20% on the first $500 you deposit, then drop to 2% after that. Others run limited time campaigns tied to a new token listing, then quietly reset the rate once the promo period ends and new depositors stop noticing.

This is why serious yield trackers separate promotional tiers from base rates. If you are comparing offers manually, always ask whether the number you are looking at is a capped introductory rate or the rate you will earn on your full balance indefinitely.

The five questions that actually determine safety

Before moving money into any earn product, run through these checks. They matter far more than the advertised APY.

- Is the platform licensed or regulated in a real jurisdiction, or does it operate offshore with no visible oversight?

- Does it publish proof of reserves or third party audits, or does it simply ask you to trust its dashboard?

- How does it generate the yield it pays out? Lending to institutions, DeFi protocols, and market making all carry very different risk profiles.

- What happened to this platform's rates during past market stress? A history of frozen withdrawals is a permanent red flag, no matter how good current rates look.

- Is the yield flexible or locked? Locked terms often pay more but remove your ability to exit if something looks wrong.

None of these questions can be answered by looking at a rate alone. They require research into the platform itself, which is exactly the step most people skip when a big number catches their eye.

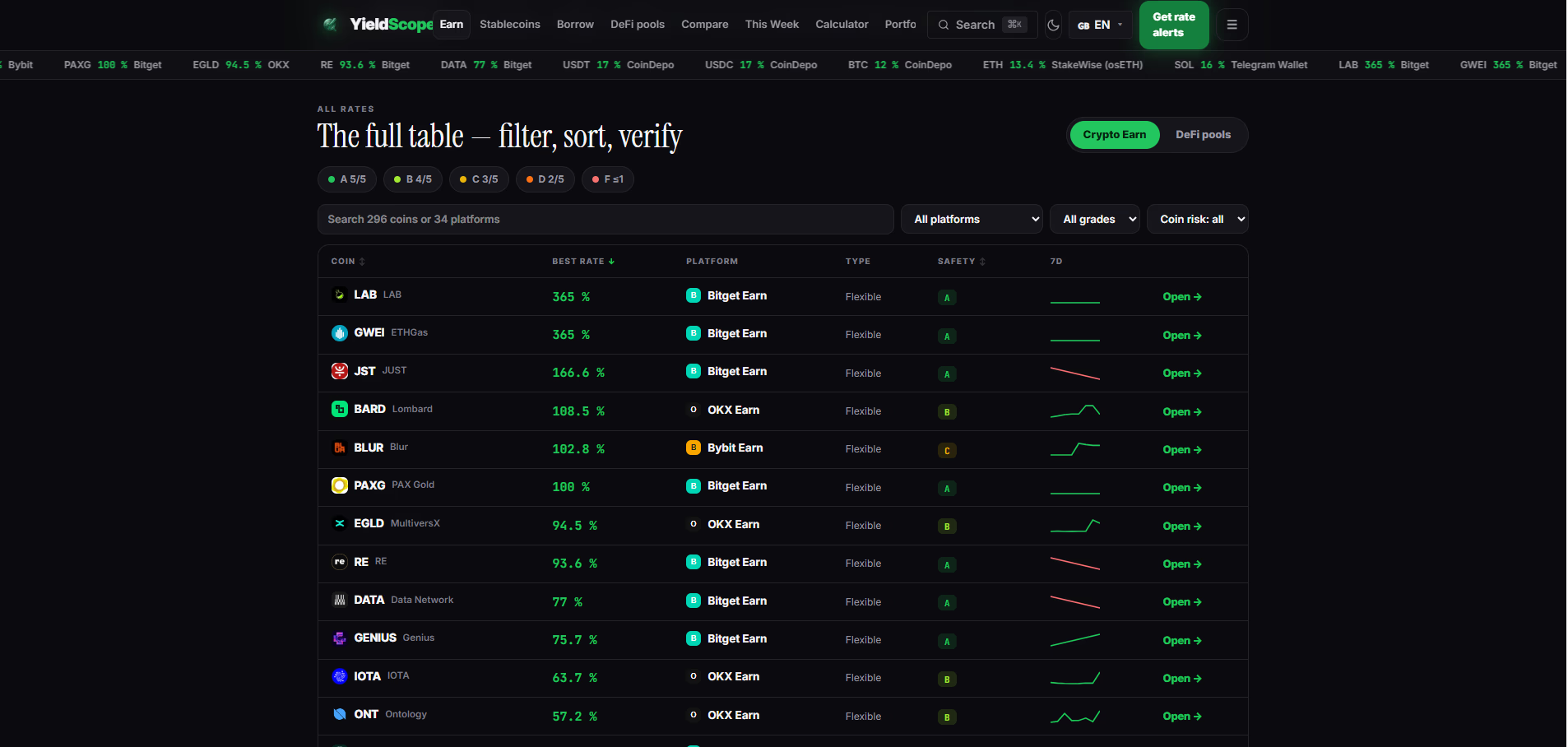

Reading a safety grade the right way

Some comparison tools now grade each platform from A to F based on public safety checks rather than just listing rates. A high grade generally reflects things like regulatory standing, reserve transparency, and a track record of honoring withdrawals. A low grade does not automatically mean a platform is a scam, but it does mean you are taking on meaningfully more risk in exchange for that extra yield.

The most useful way to use a grading system is to look at safety and rate side by side rather than sorting by rate alone. An A grade platform paying 5% and an F grade platform paying 17% on the same stablecoin are not really comparable products. One is closer to a savings account, the other is closer to a high yield bet.

Watch for rate spikes, not just rate levels

A sudden jump in an asset's advertised yield is often more telling than the number itself. When a coin's rate spikes 30, 40, or even 50 percentage points in a day, it is almost always a temporary promotion designed to pull in fresh deposits, and it tends to reset just as quickly once it has done its job. Tracking these swings over time, rather than checking a rate once and assuming it is stable, is one of the easiest ways to avoid getting pulled in right before a reset.

This is also why comparing a platform's rate history matters more than a single snapshot. A stablecoin paying a steady 5% for months tells a very different story than one that jumped from 2% to 20% last week.

Diversify instead of chasing the single highest number

Even after doing the research, it rarely makes sense to put all your stablecoins into whichever platform currently tops the leaderboard. Splitting funds across two or three platforms with solid safety grades reduces the impact if any single one runs into withdrawal issues or gets hit by a regulatory action. The extra percentage point or two you might earn by concentrating everything in the single highest payer is rarely worth the concentration risk.

A simple approach that works for most people is to keep a base allocation in the safest, most transparent option available, then allocate a smaller portion to a higher yielding platform only after confirming it passes the safety checks above.

Using a comparison tool instead of checking manually

Manually tracking rates, safety grades, and historical spikes across dozens of platforms is not realistic for most people. This is the exact gap that a live comparison dashboard like YieldScope is built to close, pulling base rates from major platforms daily, grading each one on public safety checks, and flagging unusual spikes so you are not learning about a promo reset with your own money. Rather than relying on a single platform's marketing page, a tool like this lets you see the full picture, rate, safety grade, and recent history, on one screen before you decide where to deposit.

If you want to go a step further and explore more tools built for comparing financial products and tracking opportunities like this, NxGnTools keeps a running directory worth bookmarking.

The bottom line

A safe stablecoin yield is not the one with the biggest number attached to it. It is the one backed by a platform you can verify, with a rate that has held steady rather than spiked, and with a withdrawal history that has actually been tested. Once you start checking for those things before you check the percentage, the whole process of choosing where to park stablecoins gets a lot less risky and a lot less stressful.